Looking at current account balances

/We’ve talked about current account balances before, but they are back in the news given concerns about China’s falling current account surplus.

As a reminder, the current account balance is one part of a larger balance of payments: current account + financial account + capital account + balancing item = 0. This is just the definition - it has to equal zero. And we basically can ignore the balancing item. That is really just a errors term. (This is using the IMF definition)

The current account is the trade goods and services, while the financial account is the change in international ownership of assets, while the capital account is capital transfers and the change in non-tangible assets (very roughly). But really, the balance of payments means that a current account surplus (meaning more exports than imports) funds a capital account deficit (more capital is coming in than leaving). More simply, if a country is earnings a lot from goods/services, it needs to do something with this excess money - mainly by exporting capital. And that’s just how the formula works.

Source: World Bank, chart by Vietecon.com

The funny thing is that like any equation, it can be expressed in different ways. For example, the current account can also be thought of as the country earning lots (through exports) but spending less (on imports). And this can be expressed as CA = NS - NI or current account = national savings (private and government) - national investment. That’s because if it is spending less than its earning, the difference goes into savings.

In China, we think of the current account deficit as being one of lots of exports. And the trade war has resulted in a decline in those exports. But we could also think of it as Chinese savings lots, and investing less than that (at least domestically). The recent decline in savings is generally attributed to the big government deficits (remember savings are from the private sector or the government) as part of a stimulus package.

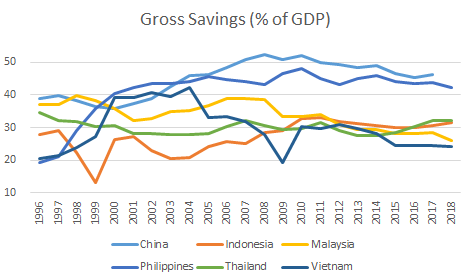

Source: World Bank, chart by Vietecon.com

If the Chinese government pulls back some of that spending, it will mean savings go up, and the current account balance will also grow. A lot of this is taken from Brad Setser’s post here. His view is that China is very unlikely to see a current account deficit because of its high savings rate.

As you can see in the chart, China has an extremely high saving rate: 45% in 2017 (no data for 2018).

This has been a criticism of China. That is forces people to save at very low rates, then it uses those savings to build up its infrastructure/exports. Low-income Chinese, through their saving, have underwritten inexpensive consumer goods for developed countries. And allowed it to make investments in its Belt and Road Initiatives and build up a massive USD dollar reserve balance.

And it is very unlikely to change in the short- to medium-term, because the Chinese is very unlikely to liberalize capital outflows (which are likely to be high) and/or its currency (which will likely depreciate, making its trade balance with the US even more positive). That means that the country will still have to buy lots of dollars and/or invest abroad in these big infrastructure projects.

Looking at Vietnam through this lens

Vietnam has a good sized current account balance of 2.4% in 2018 and 2.3% in 2017. That was better than China and only less than Malaysia and Japan.

At the same time, it’s savings aren’t as large as the rest of ASEAN, at 24%, just a bit better than the US (which has a low savings rate) and almost 20pp below the Philippines. And it is falling a bit, at least from its earlier highs.

So while exports are likely to grow as Vietnam benefits from the US-China trade war (with no end in sight), a low savings rate may hamper mean a the current account deficit. That could put pressure on the exchange rate, which we have talked about a lot.

We will have to see what happens over the next few years, as FDI in Vietnam grows. It will be interesting to see what that will do to the balance of payments.