Beyond Meat - great IPO, lousy stock?

/I have been increasingly interested in environmental issues, and sometimes I move away from Vietnam to talk about something interesting in this arena. Beyond Meat (Ticker: BYND) just IPO’ed the other day in the US. It is an alternative to meat. The first product was a hamburger made completely out of plant protein and has expanded to other meat products (sausages, ground meat). It has taken off in the US, and is now available in most grocery stores (big ones like Whole Foods, Albertson’s, Krogers, among others) and food chains (Del Taco, Carl Jr.’s).

It has competition. My favorite is Impossible Foods, which has quite a tasty burger. The big difference between them so far is that the Impossible products are only available in restaurants (but including Burger King, in the US at least), while Beyond is also available in supermarkets. Beyond’s push into restaurants is new, but they are being very aggressive (they increased their SG&A headcount by 224% in 2018).

There are a lot of reasons why I think this is interesting and important.

First, for health reasons, these foods may be better for people (excluding the much higher sodium than regular hamburgers - about 16% of a person’s daily recommended allowance). I often find “healthy” foods increase the amount of sodium to improve taste. That’s clearly what is happening here. But there is no cholesterol and they have the same amount of protein.

Second, for moral or religious reasons, people may want to decrease their consumption of animals. I have mixed feelings about this, because I am not a vegetarian, so almost anything I would say would be hypocritical. Basically, I continue to eat meat by avoiding any thought of animal welfare. But for those that care, these are a great alternative from meat.

Third, for environmental reasons, eating less meat is essential to slowing climate change. Animal agriculture is responsible for between 13-18% of greenhouse gas emissions. It’s either #2 after burning fossil fuels for energy or #3 after deforestation. Many people in developing countries have been too poor to eat red meat, and the worry is that all of these people will get richer and the amount of meat eaten (and therefore produced) will have to grow exponentially. Of course, as a Westerner, it is hypocritical of me to say “don’t do what we do," but…for the sake of the earth, don’t do what we do.

There are also companies growing meat in labs, which is another interesting solution. But so far, the plant-based alternatives that taste and look like real meat are making headway.

So back to Beyond. They had an IPO. The IPO price was $25 (at the high end of a raised range), then opened at around $46 per share. And it is now trading above $70 for a market cap of $4bn. In 2018, the company had revenue of $88m and a loss of $30m. So nice pricing for the company. Of course, people are valuing the company on expectations of strong future profits, and growth has been crazy - revenues grew 170% in 2018. And gross margin has gotten above 25%, which is quite high compared to other food manufacturers. For example, Tyson’s has a gross margin of 13%, while Hormel is just at 20% and Pilgrim’s Pride has been around 15% (although fell to 8% in 2018). So it is an exciting business.

Having said that, the valuation is crazy. There have recently been some purchases of fast growing food manufacturers. This include White Wave (which produces Silk soy milk) was bought by Danon at a 3x revenue multiple. Annies, which makes healthy frozen foods, sold to General Mills at 4x. And a bit back, Dean Foods bought Horizon (organic dairy products) for a 4x revenue multiple.

Even at a very aggressive $200m in revenues this year, Beyond would trade at 20x revenues.

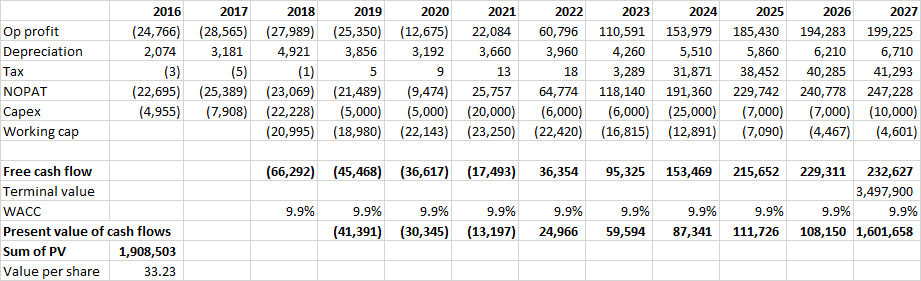

I put together a quick and dirty model with a discounted cash flow analysis. I was pretty aggressive about assumptions (CAGR of 33% through 2027 for revenue, 42% for gross profit). I also didn’t include too much capex ($91m seems reasonable given the amount of food that needs to be produced). I did use a fairly high weighted average cost of capital (WACC), but their debt rates are actually pretty high (“The interest rates on the 2018 Revolving Credit Facility and the term loans at December 31, 2018 were 6.25% and 9.50%, respectively.”), so we need to assume that equity rates would be higher.

Put all of that together, we get a value of $1.9bn in total, or $33.23 per share (see table below). So to get to $70 per share, we would have to grow revenues 41% and gross profit 50%. That’s every year for 9 years straight. Pretty intense. Or we could lower the cost of equity capital to 6.75% (which seems pretty low given an expected beta and the debt rates).

Of course, there are investors that just love growth stocks, and think that Beyond could take a much bigger share of the global meat market ($270bn in the US in 2017 or $1.4 trillion worldwide) than we are anticipating (right now much less than 1%). Or a big food conglomerate may decide that they need to make a really big move into the non-meat meat and overpay for the company.

But I don’t think that is compelling for me. I started to look into potentially buying shares in BYND, because I wanted to be a part of this trend. I feel strongly that these meat alternatives are essential for the environment. But at these valuations, it doesn’t seem like a great buy.

Source: Vietecon.com