Equity versus Debt

/I saw this article in Bloomberg about capital raising in Vietnam. Quick summary: equity raising (at least through the public markets, like IPOs or secondary transactions) have been very small, but debt has grown quickly. According to their numbers, debt issuance has been $5 billion compared to just $45m for equity raised.

A few points:

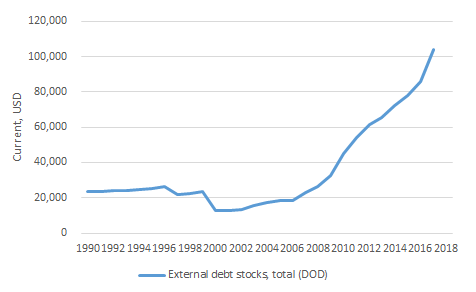

SOURCE: WORLD BANK

Debt issuance is always much bigger than equity raising. That’s the way of the world. In Vietnam, the external debt stock in 2017 was $104bn, compared to GDP of $224bn. That doesn’t include internal debt. Market cap to GDP was 52%, which is close to just the external debt of Vietnam.

It doesn’t seem like all equity investments in public companies are being counted. The article says that only $45m has been raised in equity (I assume on the stock market in IPOs or secondary offerings), but we talked two days ago about $1.5bn in capital that Vingroup raised in 2019 so far. This vastly exceeds the amount that VinGroup raised in debt ($360m according to this article). Once you add in $1.5bn to $45m, it doesn’t seem so dire.

It also discounts private equity investment. Just looking at startups, they raised $246m through June and are expected to reach $800m, according to venture capitalists. And that doesn’t count equity investments in non-startups.

I think the point of the article is true: the stock market has not been performing up to expectations. We glanced on this a few days ago when we talked about correlations. The market (as evidenced by the VNM ETF) is up 7% (good), but not as much as the S&P (20%). That’s in the context of a booming Vietnamese economy that should be boosting earnings and therefore valuations.

Debt priced in USD is rising, and that’s not necessarily good. We have talked about this before, the mismatch between currencies with so many emerging market economies issuing debt in USD, but their revenues are mostly in local currencies. I used to cover Turkey, and Turkish companies would always issue USD-denominated debt because rates were so much lower (5% vs 18%+). But the currency would then depreciate, so in TRY-terms, the debt was much more expensive. And it happened all the time. You would think they would learn! Oh, and the currency usually depreciates when the economy is doing poorly, so it’s a double whammy.

Too much USD-dollar debt outside of the US can hamper Fed policy makers. Basically, if the Fed raises rates, then these companies may face a double threat of higher interest payments in an appreciating US currency. That would then hurt the economy, which, given globalization, will likely impact the US, forcing the Fed to lower rates. Or at least that is a path. The Fed probably won’t be raising rates any time soon, but they will at some point, and companies better be prepared for it.