The State Budget

/Apropos of my post yesterday about debt, I saw this article about state budget collections in Vietnam for 2019. They were good!

Source: Ministry of Finance

Total collections were VND1,549.5 trillion or USD67.4bn. That was up 8.7%, or well above the economic growth rate of 6.8% (if you believe the World Bank) or 7.0% (if you believe the government). This means that collection has become more efficient.

This revenue resulted in a budget deficit of 3.4% of GDP, which is better than the target of 3.7%. If this continues, we will likely see a decline in the government debt/GDP figure, which would probably be appreciated by the market.

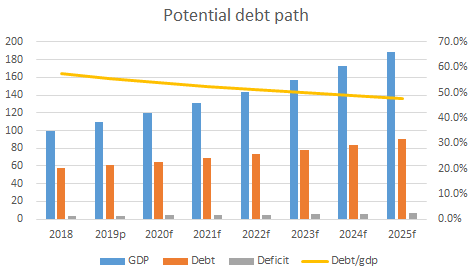

GDP indexed to 2018 = 100. Assumes 6.5% real GDP growth plus 3% inflation. Source: VIetecon.com

As I always have to remind myself, it isn’t important how much debt is added, but rather how the ratio of debt to GDP trends. For example, if GDP grows at 6.5%, inflation is 3.0%, and the deficit is no more than 3.5% of GDP, then the debt/GDP ratio will fall (see chart to the left, which shows this exact scenario). Also, inflation is generally good for borrowers - it is a transfer of wealth from lenders.

But back to collections. It is good that Vietnam was able to collect more than it expected. And it is mostly from domestic sources, so it isn’t heavily dependent on tariffs, which is probably good (they are more volatile, and we are likely to see falling tariffs collections as Vietnam signs more trade deals with Europe and TPP comes into effect).

Given strong growth, it is better for the government to collect revenues now and pay down some of its debt, so that when a crisis comes (and there is always a crisis ahead), it will have flexibility.

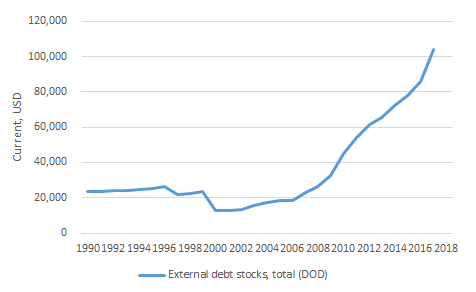

External debt stock for Vietnam. Source: World Bank

As I have written about a fair amount, I do not think that debt is all that bad. But I am worried about external debt, which has increased dramatically (see chart to the right). It stood at USD108bn at the end of 2018. I wish the government would source more debt locally, because if there is capital flight for any reason, the risks would be much lower.

Overall, with these budget figures, I am less worried about Vietnam’s debt. Although, as the World Bank said in its report, government debt is just part of the issue. We should also be monitoring private debt. The reason is that if private debts are high, companies may not be able to service these debts in a downturn. That could result in bankruptcies and layoffs. Lower debt levels means that companies can wait out the bad times.

Also, private debts can become public debts very quickly, especially within the banking system. Remember what happened in the Great Financial Crisis - large private debts were ultimately taken over by governments. A great example is Ireland, which took on all the debts of its banks, stupidly in my opinion.

Vietnam’s banking system is unlikely to face a crisis like that anytime soon, because it is heavily funded by deposits. But it is still important to think about the risks.

Next week, I hope to get back to productivity but also look at the big winners and losers of the 2019 stock market. Have a great weekend.