TNG and how markets don't move like you expect

/The more I look into the Vietnamese market, the less I know. The main thing is that Vietnamese stocks are really not expensive. I mean, some can be sort of pricey, but the P/E ratios that I have been looking at in the US or other emerging markets are very high. But the small cap stocks in Vietnam, well, they are just very cheap on a P/E basis: 3-6x. That’s nothing. That means for some companies, in 3 years, you earn back your investment. Plus, return on equity can be quite high, as we saw with MWG.

Source: Yahoo finance, chart by Vietecon.com

And today, my conceptions about the market affect of COVID-19 have been totally blown away. First, let’s set the scene. In the US, the markets are a mess. The S&P 500 is down 11% for the year as of the close yesterday (and trading down another 3.5% today when I last looked). But there are some stocks that have done well:

Zoom Technologies: Up 7.1x since the beginning of the year. This is a online video meeting platform. It is very well liked. It is profitable. And lots of people are using it now as remote work becomes important.

Co-Diagnostics, Inc: This is a company that makes tests for COVID-19. It’s up 7.6x! And no duh. It makes the thing that literally every single American wants right now.

Clorox: In the US, this is the main brand of bleach and disinfectant. It is up 12%, but on a relative basis it is up about 25% compared to the rest of the S&P, so it’s doing fine. It is a very large company (market cap of $21bn), so it has a lot of products that don’t benefit as much from the virus, and that’s probably why it didn’t rise as much as the others.

Ultimately, these moves kind of make sense. Zoom is able to sign up a lot of new businesses. A friend told me a lot of colleges are using it for teaching. And many of these are going to be sticky customers. For Co-Diagnostics, it will sell any tests that it makes immediately, and probably can require money upfront. Plus, it may be able to use whatever test they make now as a basis for other tests in the future. Clorox is going to benefit from a renewed wave of cleanliness in the US.

Source; Vietstock, chart by Vietecon.com

So I was extremely surprised to see how TNG has performed. This is a maker of surgical masks, used all over the world and based in Vietnam. It announced that its sales are up 65% in February alone! And it has lots of orders. How has see the stock performed, you ask? Not well.

In fact, it’s fallen 23% since the day before the Tet holiday. And it is down 29% yoy. So the stock isn’t all that exciting.

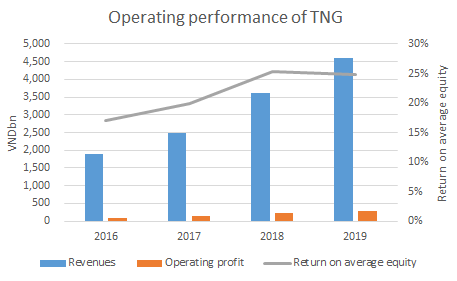

Source: TNG, vietecon.com

But the operating performance is very good: revenues up 34% annually since 2016, with gross margins mostly flat (down 60bps over the same period). Operating margins actually improved from 4.9% in 2016 to 6.3% in 2018. All of this has resulted in improving returns on equity - they were 25% in 2019.

Plus its cheap. It’s trading at less than 4x trailing P/E, and

Ultimately, the company’s performance is very good. It is a low margin business, but one that is starting to result in much higher returns. Liabilities have grown just 14% annually since 2016, compared to a 27% increase in equity. Debt to equity is high at more than 1.3x, but it has fallen from 2.1x in 2015. Basically the trends are all in its favor.

The only things that makes me nervous are:

Free cash flows aren’t great. The company probably had more cash from operations than capital expenditures (it is hard to tell from the current financials), but barely did in 2018 and didn’t before then.

Most liabilities are short-term. Short-term borrowings and leases make up 53% of all liabilities. This is down from 63% in 2016. The company is slowing moving these to long-term, but it is taking some time. And the general trend is for assets (and therefore equity) to grow much faster than liabilities.

The company doesn’t have a long track record of dividends. TNG paid a cash dividend of VND800 per share last year. (It often gives shares as dividends, which doesn’t count*.) That’s not a bad dividend at 6.2% yield. But it doesn’t have a long track record of paying the in cash.

A large number of shares being issued. This probably isn’t a big deal, but the company had less than 30m shares back in 2015 and now has 65m. Lots of these appears to be share dividends (more on this below). Management holds a third of all shares.

I think another dividend this year, say VND1,000 per share, would go a long way to quell these concerns. And if the company could move more liabilities to long term, just to ease some pressure. I think that would be helpful. Growing revenues and order book should allow this to happen.

Of course, I might be missing something obvious. Also the fact that the market cap is so low ($37m) means there probably aren’t tons of professional investors looking at it. We will have to see, but I am bullish on the stock.

* For example, say you own 100 shares, which equates to 10% of all shares, which means that there are 1,000 total shares outstanding. The company gives you a “dividend” of 1 share for every share you own. You now own 200 shares, but the total number of shares has increased to 2,000. Do the math. Yep. You still own 10%.