A few more items on MWG

/I just wanted to follow up on the MWG posts from last week and earlier this. Specifically, I want to look at capital efficiency and make sure that I’m not missing anything from the balance sheet side.

The funny thing is that I spent most of my professional life focused on the balance sheet, because I was looking at real estate, which is all about assets and how to fund those assets. Also leverage is super important. But when I look at consumer-facing companies, I look mostly at the income statement, like some sort of balance sheet-blindness.

Source: MWG, Vietecon.com

But as one investor told me, return on equity is the name of the game. If they have a high one, then it can justify a lot of sins.

So let’s look at MWG. There are a few things that I want to investigate.

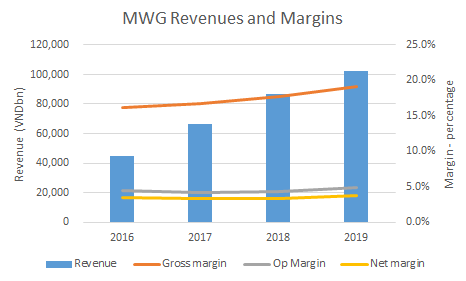

First, is the company’s operations suffering from the massive growth that it is undertaking? Short answer no. Looking at the chart to the right, gross margins have improved, and so have operating margins. In 2016, operating margin was 4.5%, and in 2019 it was 4.9%. The trend is similar with net margins.

Source: MWG, Vietecon.com

Second, is MWG able to convert accounting profits to cash? The answer is mixed. For 2017 and 2018, the company’s net cash from operations was somewhat close to its operating profit, 95% and 60%, respectively. What that means is that it was able to produce a fair amount of cash, not just accounting profits. However, in 2016, the company actually had a negative figure for net cash from operations, and that was true in 2019 as well. In both cases, it was working capital that drove down cash. More about that below.

Third, how is MWG funding its stores expansion? Mostly from operations, but not always. This is very similar to above, in that for 2017 and 2018, the company had more than enough cash to fund its capex. For example, in 2018, the company threw off VND2.3tr operating cash, and it invested only VND1.5tr in new capex. It was similar in 2017, when operating cash was VND2.7tr, and the company only spent VND2.1tr on new stores. Of course, with negative operating cash in 2016 and 2019, cap ex needed to be funded. In both years, it was funded by debt.

Source: MWG, Vietecon.com

Fourth, how good is MWG at controlling working capital? Until 2019, alright. Let’s break it up into three main buckets: accounts receivable, accounts payable and inventory.

Accounts receivable: Here the trend is MWG’s friend, in that days sales outstanding (DSOs) are actually falling from 7.5 days in 2016 to 6.0 in 2019. This means that the it only takes 6 days on average for the company to be paid for its sales.

Accounts payables: Things are good here too. Days payable are rising, which is positive. You want to get paid on time (low DSOs) but then turn around and wait a bit to pay your suppliers. At MWG, the company pays its bills on average 45 days after receiving them. This is up from 33 days back in 2016. This may not be sustainable, and it is very unlikely that they will be able to increase it anymore. But if they just keep it at this level, they will be doing fine.

Inventory: This is where it gets troublesome. Inventories are skyrocketing: from VND4.9tr in 2016 to VND25.7tr in 2019! That’s more than 5x, while sales are growing less than 4x in that same period [although growing that fast is crazy good]. Almost every category has gone up: electronic equipment, mobile phones. Plus the company added watches to the tune of VND573bn. The number of stores has increased a lot, and you have to fill them at the beginning, so it could be that initial stock. But it now takes 95 days for the inventory to turn over, or once a quarter. That’s way too high, especially for a company with 10% of its sales in very perishable groceries (although to be fair, most of the increase in inventory comes from nonperishables).

Source: MWG, Vietecon.com

This is my biggest concern over MWG: the increase in inventory is crazy. It grew VND8.4tr in 2019 alone, and all of that was in 4Q. There’s no real explanation in the financials, but maybe there will be something in the annual report.

Fifth, is debt climbing too quickly? Not really, but it’s complicated. Basically, the company’s debt to equity seems high at 1.2x debt-to-equity. Both equity and debt have been trending up, but debt really grew in 2019. However, when compared to EBITDA, it isn’t too bad. Debt-to-EBITDA is still 2.2x. But again, it comes back to that working capital. If working capital had been just a bit better, then the company wouldn’t have had to get so much new debt. But it did. This is a metric that I am going to watch closely, but I think that if working capital needs improve, then its very unlikely that the company will face stress around its debt. Let’s just hope COVID-19 doesn’t last too long!

Source: MWG, Vietecon.com

Finally, how does return on equity stack up? Very good. Basically, the company has amazing returns on equity (RoE): 36% for 2019. They have been falling, though. Back in 2016, RoE was 50%. That’s crazy high. Of course, a way to raise return on equity is to pay out dividends. Equity would fall, thereby raising RoE. Unfortunately, if you have cash needs, you can’t pay that dividend. And that gets us back to the increase in inventory.

The company is doing quite well at managing its growth, except for inventory. But I suspect that part of the increase in inventory was a one-time effect. I would have to do a bit more research to be sure. Unfortunately, while Tet sales were good, the company may end 1Q with high inventories as well, because of COVID-19. Ultimately, though, the company has the ability to get over this hiccup.

Bottom line, except for inventory, everything is going quite well. I haven’t changed my mind on MWG yet. Give me time!