Where stocks stand now...

/Great news, 4 days of no new cases!

Now on to the news…I need to follow up on Friday’s post about debt. Reminder: Post-COVID, I believe that companies will decrease debt and leverage in order to be more resilient going forward, but potentially at the cost of equity returns. Debt is almost always cheaper than equity, and so, all else being equal, more equity means lower returns for those equity holders.

And probably we need to widen the discussion on debt to the country and emerging markets as a whole. This Odd Lots podcast has an interesting discussion on how countries may try to beef up reserves and move away from dollar debt (and debt overall), which would probably prolong any recession as spending falls. Someone’s consumption is another person’s income. If you cut back consumption to pay off debt, then someone else’s income falls, which forces them to cut back spending too…

Source: Vietstock.vn, Bloomberg

That’s something to think about, but today, I wanted to look at where we are in terms of stocks. Both the indices and individual stocks.

First, for the indices:

VNM ETF is down about 23%, much worse than the local indices. That’s partly due to currency issues: the KRW is down 5.1% compared to USD since the beginning of the year and the VND down 1.2%.

The VN Index (which represents stocks in HCMC) is down 17%, about the same as Japan.

Hanoi, which is about a tenth of the size of HCMC, is up 7%, but that’s probably just because of a few stocks. I wouldn’t read too much into it.

The S&P is down 12%, and the NASDAQ (which is composed mostly of tech stocks) is only down 3% YTD. This surprises me, because I feel like the US has done such a bad job combating COVID-19, but the stock market is one of the better ones. Helps that the Fed has been so aggressive.

The UK Index has performed particularly poorly, even with massive stimulus there. Seems like with Brexit coming up, the UK markets could be for a rough few years.

I also want to look at individual stocks. I looked at all the stocks in the VNM ETF (which gives us a good range of large market cap stocks) and ones that are widely held by local funds (see my consensus post here).

Source: Vietstock.vn, Bloomberg

Diving into some stocks, I was very surprised by a few individual ones. I am going to break these down into groupings in order to better show performance in charts (right). Let’s start with the biggest companies first.

All of them fell, and most between 10-20%. Two companies somewhat outperofrmed: Vietjet (-8%) and Hao Phat (-10%, but up 2.4% just today).

I would think that Vinamilk would have done better - its a staple, more people eating at home, etc. It didn’t, probably because the underlying business is growing slower (saturation in Vietnam), plus its expansions outside (re: China) are put on hold. And it’s still not that cheap at 18x P/E (16.5x forward P/E).

Vincom Retail performed much worse than the other biggest companies, probably because it is dependent on retail, which is not happening. As a reminder, Vingroup owns a majority stake in VRE.

Source: Bloomberg, Vietstock.vn

The second set of stocks shows a wider range of performance, from +5% for MSN and -78% for Faros (ROS).

MSN had performed so poorly late last year, plus it is in grocery. Those two things combined means that isn’t so surprising that it is doing well. Obviously the market viewed its tie up with Vincommerce as a bad deal, but it’s redeemed itself a bit.

Faros is down tons, after a steady and massive decline in 2019 (-42% in 2H). It is also out of the VNM ETF. This was a long time coming…

TCH (Hoang Huy, which does real estate, trucking and finance) saw a massive rise in 2H2019 (+50%), so it is actually just back to where it was for most of 2019.

Source: Bloomberg, Vietstock.vn

The third set of stocks are back to less variation.

SCS is holding up the best, helped by very poor performance in 2H2019 (-24%). Also, you would think that logistics would hold up, given still strong exports/imports plus more ecommercee.

My beloved MWG is down a lot, and I just don’t get it. Yes, 2/3rds of its business is closed (!), but the 1/3rd should be doing very well. And it will recover. But maybe I’m just talking my book.

I could see FPT both benefiting and being hurt by this. Companies look to outsource to save money when times are tough, but also new contracts are probably not being signed. It will be interesting to see how the company looks post-COVID.

Source: Bloomberg

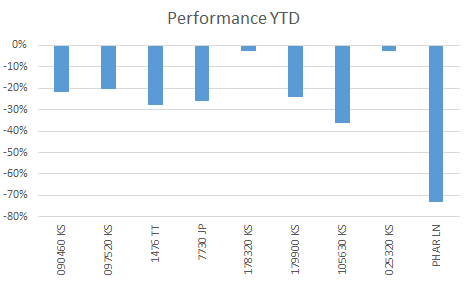

The fourth and final set of stocks is foreign companies with lots of activity in Vietnam.

Pharos Energy is the worst performer, which isn’t really a surprise. It is a small oil & gas producer that made a loss last year. Luckily, it’s balance sheet seems alright, so it will probably stay in business, but oil at $26 (Brent) doesn’t help.

Seojin Systems (178320 KS) is basically flat. So is Synopex (025320 KS). Both of them are suppliers for Samsung, which is down about 10% (2.5% today). So I guess the view is that Samsung will have to continue to buy supplies, which seems like a good bet.

The rest of the stocks are mostly in line except for Hansae (105630 KS), a very large apparel manufacturer. It’s down 36%. The company was unprofitable last year, and the stock was already down because of this. A hoped for turnaround seems unlikely in the current climate.

So overall, very few Vietnamese stocks have been able to perform well during the crisis, even ones that would seem to do well.