Banks and more capital

/Following up on our discussion yesterday about interest rates, one of the impacts of lower rates will be less income for banks. Banks are already in turmoil because of COVID-19 for a number of reasons.

The first is that lower interest rates mean less income, because many loans are repriced quickly (they are floating, meaning a fixed spread over short-term interest rates). Meanwhile, the cost of money (savings rates, etc) don’t fall as quickly.

Source: SBV

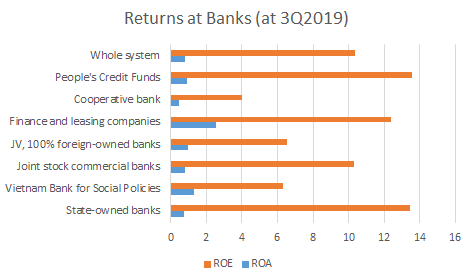

Returns at Vietnamese banks are already kind of low. The whole system has a return on equity (RoE) of 10.37% (as at 3Q2019), while the US system had an RoE of 11.67% in the same quarter. Returns in the emerging parts of Europe are also higher than Vietnam. Vietnam should have a higher cost of capital, so those returns look less exciting.

The state-owned banks (which include Vietinbank and Vietcombank, both of which are public) are doing the best with an RoE of 13.5%. Surprisingly the JVs and foreign-owned banks are not doing that well.

Source: SBV

Another impact is higher bad loans. These return figures are from 3Q2019, and it looks like returns are going to get worse from here. The reason is that non-performing loans (NPLs) are very likely to increase. They had been trending down, as can be seen in the chart to the right. The government and SBV have really tried to bring down NPLs.

Source: Vietstock.com.vn

This will likely rise again. According to Fitch:

Fitch-rated local banks* have reported a 45% surge in past-due loans in 1Q20 relative to end-2019 as the coronavirus takes a toll on the economy

We have already started to see a small increase in NPLs in 1Q2020. It varies a lot. VPB saw a 61bp decrease in NPLs, while CTG saw a 67bp increase. Out of the big state-owned banks, VCB increased its provisions 43%, while CTG increased it 36%. Note that VCB has a lower NPL than CTG at 0.82% vs 1.83%.

Of course, the full impact of COVID-19 will take a while, so we will likely see NPLs increase for all banks. Retail loans have increased dramatically over the past few years, so if consumers start to feel stress, banks could suffer. Most of these retail loans appear to be mortgages and personal business loans secured through property. I will be following property values to see the full impact on banks.

Unfortunately, for the system overall, there was already a need to increase capital. I wrote about this back in October 2019, when I quoted Moody’s and Fitch reports that said Vietnamese banks need $4-9bn in additional capital to meet Basel II requirements and grow. To put that in context, that’s 2-3% of GDP.

The capital adequacy ratio published by the SBV has hovered around 12% since November 2018 (the last date I have), but state-owned banks and joint stock commercial banks have been well below that level.

Fitch says that potentially NPLs could go as high as 6-9%, which would a massive jump and really hurt capital adequacy ratio. That’s really the worst case, while Fitch’s base case isn’t that bad. The ratings agency thinks that the majority of banks will not have problems meeting the 8% CAR required by Basel II.

One final point I would make is that we want banks to lend money right now. And we do not want them to come after borrowers right now. But unless the SBV relaxes some of its rules, they might be forced to. And if there is general deleveraging in the economy, that’s not going to be great for growth.

* Fitch-rated local banks include: Vietcombank, Military Commercial Joint Stock Bank, Vietinbank and Asia Commercial Joint Stock Bank.