Stock market - bad results and illiquid

/

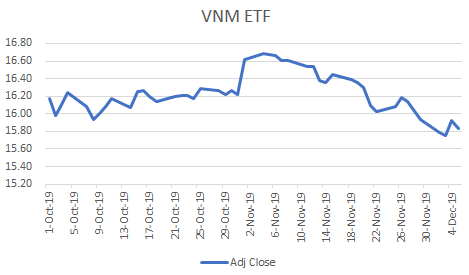

Source: Yahoo finance

CORRECTION: Below I quoted a figure from Dr. Oliver Massmann. I incorrectly spelled his name and also didn’t mention that he has a PHD from European Global School. I regret the error.

The market has been crappy for the past month. Basically right after I wrote my post on contrarianism (here) the market started to fall. The Vietnam ETF was moving up in line with the S&P500, but that has diverged completely. The S&P rose 5.9% since Oct 1, compared to VNM’s fall of 2.1%.

Now there are a few articles (here, here and here) look at the market where it is now. Luckily, they don’t try to give a fake reason why the market when up or down: articles like that are dumb. These articles actually focused on liquidity issues, which is more interesting.

Liquidity in the Vietnamese markets is not good. To give you a sense of scale: in a randomly chosen week in November, only $218m shares were traded on the Ho Chi Minh Stock Exchange. And I have looked at Vingroup, the largest stock, previously and found that it trades less than $3m a day. When I was an equity analyst, most of my clients, who were looking at emerging markets only, would only invest in stocks that traded $5m a day. No Vietnamese stock meets this regularly!

Why is there low liquidity?

FOL: Lots of stocks are at the foreign ownership limits (FOL) or are close to those limits. Many companies have a limit of 49%, even thought they don’t have to. According to David Harrison of Mayer Brown: “By April last year, two years after the passing of Decree 60 [which allows higher FOLs], only 20 out of 700 firms trading on the two bourses had abandoned the 49 per cent FOL.” Some sectors (I’m looking at you, banks and aviators), the limits are 30%, which is extremely low.

There has been talk about this changing, but I am just not sure. For example, the central bank just issued a new rule about payment systems, putting the limit at 49% (previously there was no limit), so it’s not like things are loosening daily.

Free float: Free float is also limited for many companies, which is a legacy of having lots of closely-held or government enterprises.

ETF and foreign owners: The main ETF for Vietnam (VNM ETF), which isn’t that large but is meaningful at $443m in assets, barely changes its holdings, providing zero liquidity. The articles linked to above also talk about how lots of the foreign owners are long-term holders, which isn’t great for liquidity either.

Privatization: There have been big hopes that the government would follow through on its privatization plans ($2.6bn or VND60tr from 2017-2020). This year only $147m has been completed, and last year less than $500m., according to Bloomberg. Every year, the state has fallen short on the number of companies privatized: 17 out of 135 in 2017 and 51 out of 181 in 2018. The market expected more privatizations/listings, especially of big companies, that could be players in the stock markets. This hasn’t happened.

What could change?

First, privatization is ongoing, albeit slowly. We could see a pick up in pace here, especially if the government decides it needs more money to invest in infrastructure while keeping its debt levels down.

Second, there is a draft law (published earlier this year) that would allow 100% FOL. There is a discussion of it here and here. My reading is that the FOL would default to 100% if there were no other restriction. Much of this is due to the treaties signed by Vietnam (CPTPP, EVIPA). So it is very possible we will see a change in FOL sometime soon as these treaties take effect.

Why does liquidity matter?

Investors are concerned about stocks with low liquidity because it means they can’t easily get their money out. This is not an issue for retail investors, but let’s say you are a fund manager that wants to invest in Vingroup and you manage $500m in emerging market assets. You want to have a sizable position in the company, let’s say $10m, which still equates to just 2% of your total portfolio. But it would take you 3 full days of trading to get out of your position, if something bad happened. That’s a long time. And it would actually take much longer, because if everyone knew you were trading that much, it would drive down the stock.

Whereas if Vingroup traded $100m a day, you could slowly pull out a few million every day and the price impact would be minimal.

If FOL is raised, then we could also see Vietnam become more competitive for MSCI’s Emerging Market index, attracting all of the fund managers who are investing in emerging markets. Right now Vietnam is in MSCI’s Frontier Market index

Emerging markets index or frontier - what’s better?

A bit of background here. Lots of money follows indexes. Index funds do - it’s right there in the name. And mutual funds are benchmarked against an index. Hedge funds too, many times. The main player in indices is MSCI, and its emerging market (EM) indices are the most popular among EM indices. When MSCI adds something to the market (like China), then all the firms that track the index have to go buy those stocks.

For example, recently, Saudi was added to the MSCI Emerging Markets index, and it saw massive infows of foreign investment. The estimate of potential investment for Vietnam is $15bn, according to Dr. Oliver Massmann from Duane Morris.

I would say two things:

1) Right now the MSCI Frontier Markets index weights Vietnam 17%. However, Kuwait, which makes up 37% of the index, is moving to the Emerging Markets index. If no other changes were make, Vietnam’s weight would move to 27% automatically. No matter what, we are going to see inflows into Vietnam next year when Kuwait moves out of the index. However, ETFs that follow this MSCI Frontier Index have assets of just around $1bn, and what I hear from market participants is that there are very few funds that follow frontier. It is just out of style right now, unfortunately.

2) Emerging market funds are a magnitude larger, so it makes more sense to be in the emerging markets index. There is more than $150bn in money following the MSCI emerging market index in ETFs alone, not counting the emerging market mutual funds.

The Philippines currently have a 1% weighting, which is tiny. It’s the smallest weighting that is still broken out. If Vietnam got just that 1%, it would attract $1.5bn in new inflows, and likely much more. That’s more than in all of the frontier ETFs.

To be fair, sometimes investor focus is helpful, and there would be a much bigger focus on Vietnam in the Frontier Index than in the EM Index.

Overall, though, Vietnam should shoot for MSCI Emerging status. To do that, it should increase liquidity in the market by a) privatizing SEOs, b) raising FOLs, and c) trying to free up float. If the market was able to do all that, it would attract billions in new investment, a good part of which would be long term.