Follow up on liquidity

/One thing I found interesting when I was looking into liquidity issues in Vietnam is that there has been a bit of work done on it. Specifically, I found this paper that looked at how asset managers manage liquidity.

The takeaway from the paper is that portfolio managers actually do a pretty good job of forecasting liquidity. As we talked about on Friday, asset managers care a lot about liquidity, because it can matter whether they sell at a profit or a loss (or usually they can sell for a small loss or an even bigger loss). They need to take a position on liquidity in their portfolio and in specific stocks. If a stock is illiquid, then they will only buy it if it is exceptionally cheap.

This paper says that portfolio managers in Thailand, Malaysia and Indonesia, as in developed markets, are good at forecasting liquidity. When you go a bit deeper into the data, though, the insight actually becomes a bit less interesting. Actually, portfolio managers that have good returns are also good at judging liquidity.

“Our finding here is consistence with the prior literature in that the good performance funds can generate the positive abnormal return [from liquidity], while the poor performance funds cannot generate abnormal return to the investor.”

And:

“The result […] shows that the best performance portfolios successfully time the market liquidity, while the worst performing portfolio fail to do so in all markets. Furthermore, the best performing portfolios demonstrates a positive abnormal return in all panels as we found in previous section.”

So, get this: if you are a good portfolio manager, one of the things you do well, is to judge liquidity of your stocks. And if you are a bad portfolio manager, one of the things you do bad, is to not understand the importance of liquidity for your stocks.

Not sure what you can learn from this, except if you are a portfolio manager, be better at your job.

Liquidity in Vietnam

Source: Vietstock.com, chart and calculations by Vietecon.com

Also, I wanted to add a little more to what I said about Vietnam on Friday. Specifically, I said that there are no stocks that big fund managers would buy. I was looking at some old data, so I wanted to update a little. So I took today’s trades and put together a chart that shows trading value per stock.

As you can see, a large portion of stocks (53 in total) didn’t trade at all. Then another 274 stocks didn’t trade more than $0.5m. In total, 19 stocks trade more than $1m today, 3 more than $5m, and just two (ROS and VRE) over $10m. ROS traded almost $30m worth of stock, or almost 5% of its market cap. That’s crazy and is not a positive thing, in my view. It means that there are a lot of retail traders. Actually, scratch that, that could very well mean that there is an opportunity there.

Source: Vietstock.com, chart and calculations by VIETECON.com

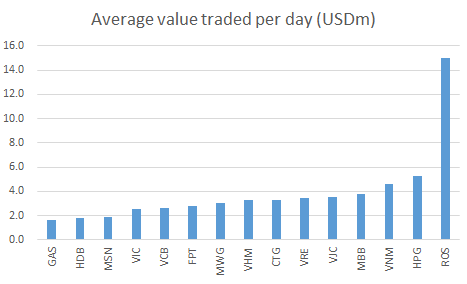

And today is not out of the ordinary. I looked at the top 20 traded stocks (by value) over the past year. The chart to the left shows the top 15 (since I didn’t look at all stocks, I am pretty sure this is the top 15, but one or two may have escaped me).

You can see that ROS is well above there rest. On average, it has traded $15m worth of stock, equating to 2.5% of its current market cap. It’s been on a continuous downtrend and has lost about a third of its value over the past year, so it wouldn’t look as bad if we looked at start of period market cap.

Anyway, the funny thing is that VIC, VinGroup, the largest stock in the market by market cap ($16.8bn) trades just $2.5m a day on average. Only HPG and the aforementioned ROS hit my $5m mark, although VNM is very close. Outside of the top 15, there are only 3 more that trade more than $1m a day (again there may be a few more that do that I didn’t catch).

Tying it all up

I don’t have the time to look at value traded in the three markets, Malaysia, Indonesia and Thailand, that are referenced in the research linked to at the top, but it is more than Vietnam. So investors in Vietnam need to focus even more on liquidity, since they can’t take it for granted. And the liquidity premium should be great for Vietnam than for other ASEAN markets. Put in simple terms, Vietnamese shares must be cheaper than other ASEAN stocks because they are more illiquid.

Again this points to the need to make reforms around ownership (both foreign and free float). Why? Well, if this liquidity premium goes away, then share prices will rise, and companies will be able to raise more money than they can currently. That means more investment, both foreign and domestic. Which is a good thing.