Quick look at value in Vingroup

/Today, I wanted to highlight a few things following on our discussion of Vingroup yesterday.

Source: Vingroup, Vietstock.vn, chart by Vietecon.com

Specifically, I wanted to talk about how to look at the valuation of Vingroup. What I mean by that is that Vingroup is ultimately a conglomerate with a number of pieces, some of which fit together better than others. It also owns majority stakes in two publicly-traded real estate companies, Vincom Retail and VinHomes. These two actually have the most synergies - both are developers, one of commercial and one of residential.

It is very easy to see how much these two make up to Vingroup’s overall value, because they are publicly traded.

VIC owns 56.86% of VHM, for a value of $6.6bn.

It owns 73.66% of VRE worth $2.0bn.

Source: Vingroup, chart by Vietecon.com

In total that means out of a market cap of $14bn, 59% is from these two publicly-traded stocks. In that regard, VIC is a real estate company.

Back in my equity research days, I had to do so many sum-of-the-parts valuations. These are helpful in really providing clarity on where value is coming from. For instance, it is now easier to look at the rest of the business and see if the value implied by the market cap makes sense. Are the car and phone businesses, along with everything else, worth more than $5.8bn? Plus, they have options worth $370m as of the end of 1Q from the sale of Vincommerce to Masan? That’s 6% of the value too?

It can be hard to value each of these parts, so the publicly-traded parts give a way to back into valuations of things that are less transparent.

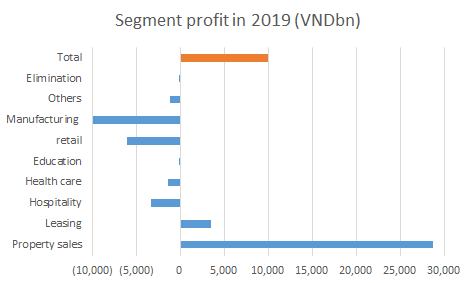

Source: Vingroup, chart by Vietecon.com

Looking at the segments, property and leasing make up 56% of total sales, plus all of the profits. (!) In fact, all of the other segments are money losing, including hospitality, which is particularly weird to me (free cash flow here is still negative even after adding back depreciation).

Of course looking at profit for segments that are very nascent (like cars and phones, which just started production last year) is not totally fair. We also need to look at the assets and the equity of these segments.

Source: Vingroup, chart by Vietecon.com

At the end of 2019, total equity of these other segments totaled VND136tr ($5.9bn), or almost exactly what the value implied by the sum-of-the-parts. So P/B is something like 1.0x for the non-publicly traded assets. Not sure what to think about it. It doesn’t look like it is heavily overvalued, but at the same time, it isn’t super cheap. Plus, most people include a discount to the valuation to account for the conglomerate nature.

This is the problem with conglomerates, sometimes the sum of the parts is worth more than the whole, at least in the market’s view. Plus there are so many ways to look at them. It would take more than just this one blog post to get to the bottom of it.

But at first glance, I think we can see that its not super easy to figure out the true value of Vingroup. If you are comfortable with the market prices for VRE and VHM, then you still have to do a lot of work on the rest of the business to see real upside.

This is not always the case. Back in my old days, the sum-of-the-parts for Emaar showed that the publicly-traded parts were worth something like 70% (making up the numbers a bit here), and the company still had assets and revenues many, many multiples of that value. It was a clear buying opportunity.

Unfortunately, for Vingroup, we can’t say anything with that kind of certainty.

Ok. Enough for today. More on real estate tomorrow.